FLY OFF THE HANDLE

When two Boeing jets crashed a few years ago, a wave of intense regulatory attention followed. Investigations were launched, approvals were delayed, and software was re-tooled. And yet, despite all this, Boeing somehow retained the power to inspect its own planes. This perhaps has something to do with the fact that the aerospace industry is highly concentrated, and powerful companies tend, over time, to build the political power necessary to maintain a high degree of influence over their regulators.

Now, after the recent near-disaster when a plug door blew out of a Boeing fuselage soon after takeoff, federal agencies are reportedly “considering” whether to remove Boeing’s right to inspect its own planes. Instead, they’re “exploring” options for third-party inspections — that is, they’re pondering whether or not somebody besides Beoing should determine whether Boeing’s planes are in compliance with the rules. While this is pretty obviously a good step… how many visible failures of deregulation do we need to witness before we stop trusting companies to regulate their own behavior? How are we still at this point, and how on earth is this still a question?

Make it make sense.

don’t think political leaders care about them, according to a new Axios poll. The sentiment is overwhelming across all demographic groups.

in pension funds have been granted to 3M CEO Mike Roman since he was hired as CEO in 2018. The company recently announced they are suspending company pension plans for thousands of non-unionized workers who are not the CEO.

is owned by the richest 10% of the country. While many people own a small amount of stock, mostly through retirement plans, these holdings are dwarfed by the amount of stock owned by the wealthy few.

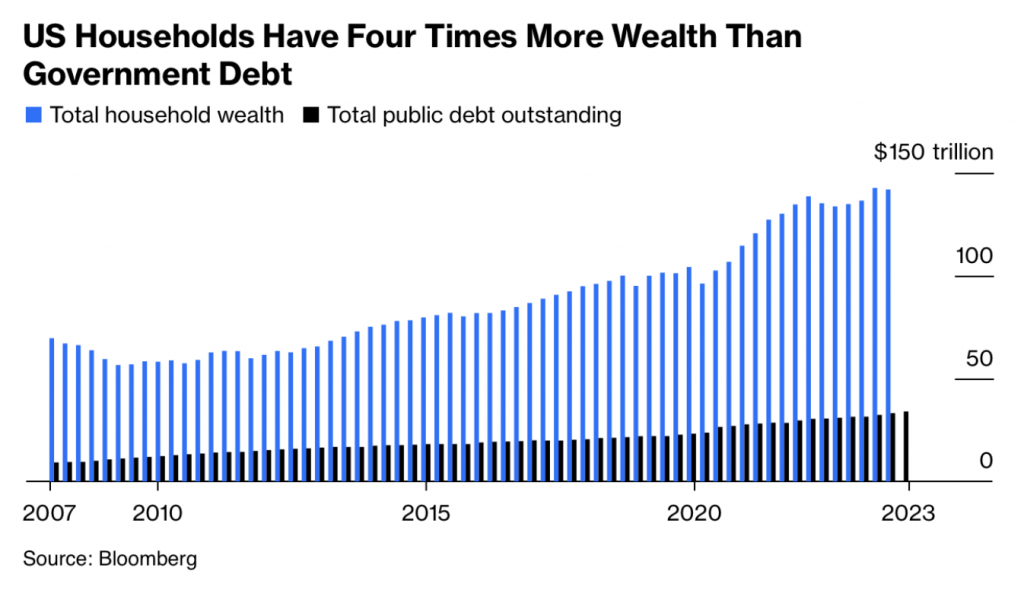

The Federal budgets approved by Congress regularly provide for collecting less money in taxes than the government spends, which means the national debt keeps on rising. And this, in turn, tends to produce a corresponding increase in the number of articles in which neoliberal commentators wring their hands about the fact that the national debt is rising. But as economist Claudia Sahm argues in Bloomberg with welcome lucidity: debt in itself is not necessarily good or bad. What matters is what the money is spent on, and what kind of return it provides.

The scale also matters. And while $34 trillion — the current total size of the US debt — is a lot of money, the cost of interest payments on the debt remains relatively low compared to just a few decades ago. The scale of the debt also matters, and other similarly big numbers are involved in that kind of comparison. As Sahm’s graph below shows, the total US debt as a portion of the total wealth held by Americans remains quite manageable. The point being: we can absolutely afford to continue to spend money on productive public investments — in fact, it’s the most important thing we can do with our national wealth.

It’s quite a bold claim: Ellie Quinlan Houghtaling writes in the Washington Monthly that despite a lack of public attention to the policy solution, “Joe Biden Has Solved the Student Debt Crisis.” But this is more than clickbait: the writer goes on to make a strong argument that the SAVE payment plan rolled out by the Biden administration effectively addresses the biggest concerns about student debt by lowering payments, tying those payments to disposable income, and automatically forgiving any remaining debt after 10 – 20 years.

No, this isn’t a comprehensive debt holiday, and the SAVE plan does not offer borrowers the pleasure of seeing their principal dramatically marked down from one day to the next. But it does make student debt far less of a burden for borrowers — and even less of a thing to think about. Which is perhaps why this major policy change in how student debt is administered hasn’t gotten the attention it deserves: it deals with the problem on a month-to-month and year-to-year basis, instead of doing it with a single stroke of the pen, a single act of Congress, or a single Supreme Court ruling. It’s a public relations challenge for certain, and that has economic implications as well as political ones: the biggest catch is that borrowers need to apply for this payment plan in order to receive its benefits.

What did you think? Choose a reaction:

Civic Action

119 1st Avenue South Suite 320

Seattle, WA 98014

United States