FEATHER IN THEIR CAP

When the Consumer Financial Protection Bureau announced a strict $8 cap on credit card late fees, which will save consumers $10 billion a year, the big bank lobbying operation kicked into gear. The financial industry is a huge source of political donations, so no surprise that they were able to get some of their allies in Congress to push back against the cap, trumpeting some good old fashioned Corporate Bullshit about how reducing late fees will actually hurt people who pay late, and/or bring on a plague of locusts, etc., etc.

But of course, eliminating junk fees is wildly popular, with one poll finding support hitting 80% of the American people, including 72% of Republicans. And the $8 figure isn’t some made up number — it was calculated by the CFPB based on the actual financial cost incurred by credit card issuers when customers pay late. Now, if you’re a politician who’s opposed to a rational, thoughtful, popular policy, you think you’d at least have the wisdom to be quiet about it. But instead, a group of Congressional Republicans is pushing for a vote on the late fee cap, bizarrely seeking to have elected officials go on record about whether they support credit card companies’ ability to gouge customers out of billions of dollars. When this is who you are and what you stand for… why on earth wouldn’t you try to keep that quiet?

Make it make sense.

in Chattanooga, Tennessee, are set to vote this week on joining the United Auto Workers union, after organizing around issues including restrictive sick leave policies, mandatory overtime, and low pay. If they succeed, these workers would be the first at an auto plant in the US South to vote to unionize since the 1940s.

don’t believe they’ll ever own a home, a figure which is up sharply from last year, according to a Redfin survey. High mortgage rates, high home prices, and soaring rents have left aspiring homebuyers in a triple bind.

net interest income was booked by Wells Fargo this quarter, a decline they attributed to consumers seeking high-yield savings accounts instead of letting their money sit in checking or savings accounts. But don’t worry, they also saw their investment banking income almost double.

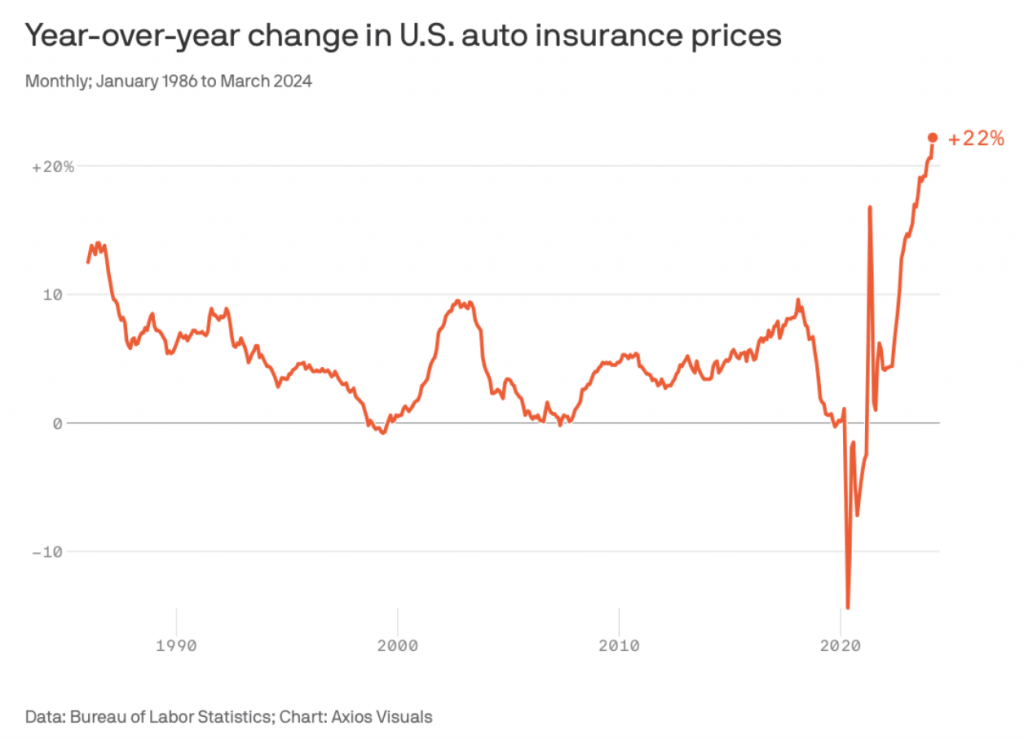

The rate of price increases has generally moderated over the past year or so, and most people’s wages have caught up. But there are a few items where prices continue to jump — including car insurance… which is 22% more expensive than it was last year.

It’s possible to offer reasonable-sounding reasons for the increase. For one, average car prices are up by $10,000 since before the pandemic — and used car prices have jumped too -—so the cost of replacing a vehicle is much higher than it used to be, and that’s a important factor for insurance companies. The cost to fix a car has also jumped, in part due to a strong labor market that left people with repair skills well-positioned to negotiate higher pay. Car crashes are becoming more frequent, too. But nonetheless, it’s still startling to see this plot of just how rapidly car insurance companies have raised their prices for what’s effectively a necessity, and tough to swallow that idea that isn’t just another example of corporate greedflation.

For all the constant political conversation about what should or should not be done to hold down the cost of Social Security, very little is ever discussed about the budgetary cost of subsidizing the retirement savings of higher-income people. In fact, as Benjamin Guggenheim details in a valuable Politico piece, you probably didn’t hear about the bill which recently passed Congress that increased the tax subsidy to IRAs and other private retirement savings accounts by $282 billion — because it passed very quietly, with very little opposition, thanks to a very well-funded push from the financial industry.

Guggenheim details at length how we got to this point, and what’s at stake when we talk (and don’t talk) about retirement benefits in this way. And what it all boils down to is that there’s no good reason why everyone in DC has an opinion about fixing Social Security, while hardly anyone seems to be even tracking the cost of providing tax breaks to wealthy people who can afford to put aside a half-million dollars a year for retirement.

What did you think? Choose a reaction:

Civic Action

119 1st Avenue South Suite 320

Seattle, WA 98014

United States